This is the guide I wish I had when I was first poking around careers in affordable housing. Whether you're a student thinking about real estate, planning, or policy, or a working professional looking to pivot into something with more purpose, you're in the right place. I'm going to walk you through the major lanes in the LIHTC (Low-Income Housing Tax Credit) world: developers, investors and syndicators, lenders, property management and compliance, government, and everything in between (the accountants, lawyers, consultants, architects, and other vendors who make deals happen, and bill for it). Who hires, what the jobs look like, what they pay, and how to get your foot in the door.

I didn't plan on a career in housing. I was on the FX sales and trading desk at Citi in London when I came across a $2.5 billion social bond financing affordable housing, and that one deal sent me down a rabbit hole. I ended up at Citi Community Capital on the lending side, then moved over to development, and I built LIHTC Leaders because this guide is the one I wish existed when I started.

Housing is its own world. It's commercial real estate, but with a government component baked into nearly every deal. Tax credits, regulated rents, federal programs, state allocations. That changes the work, the players, and the kind of people who end up doing it. It's a double bottom line business: financial return and social impact. People in the industry sometimes call themselves "housers." So maybe you're thinking about becoming one too?

If you're searching for affordable housing jobs, the hardest part is often knowing what to search for. The industry uses titles like development analyst, LIHTC underwriter, asset manager, compliance specialist, production analyst, HFA program analyst, housing program specialist. None of those tell you much from the outside. This guide breaks down what they mean, where they fit, and which one might be right for you.

What's Inside

The Affordable Housing Industry: Big Picture

Affordable Housing Developers: The Builders

LIHTC Investors and Syndicators: The Equity Side

Affordable Housing Lenders: The Debt Side

Property Management, Compliance, and Operations

Government and Public Sector: Where the Programs Come From

The Affordable Housing Industry: Big Picture

Affordable housing isn't one neat career ladder. It's an ecosystem with a lot of interconnected players, and once you see how they connect, the rest of this guide gets easier.

Cities need housing. Developers build and preserve that housing. But developers don't have all the money sitting in their bank account, so they need investors (who provide the equity, usually through tax credits) and lenders (who provide the debt). Why do those investors and lenders show up? A few reasons. Sometimes it's regulation. There's a federal law called the Community Reinvestment Act, or CRA, that basically says: if you're a bank taking deposits from a community, you have to put money back into it. Affordable housing is one of the cleanest ways to check that box. Sometimes it's financial return. Sometimes it's mission. Often it's all three at once.

Government at every level (federal, state, local) creates the programs and incentives that make all of this possible. Tax credits, grants, bond financing, zoning approvals, regulatory oversight. Then you've got the people who keep it running after the ribbon is cut: property managers operating the buildings, compliance professionals making sure the rules are followed, and service providers supporting residents directly.

One way to think about it: there are ownership roles (developers and sponsors who control the property and take on the risk) and non-ownership roles (everyone else who supports, finances, regulates, or services it). That simple divide helps you place where different jobs sit.

You'll see both for-profit and nonprofit players throughout. For-profit developers, lenders, and syndicators are driven by financial return, though many are also genuinely mission-aligned. Nonprofits like community development corporations, national intermediaries (Enterprise, LISC), faith-based groups, and philanthropies are mission-first. Both types work side by side, and you'll find career opportunities at each.

One last distinction worth knowing. "Affordable housing" with a capital A is housing made affordable through subsidies, government programs, or tax credits. The biggest program is the IRS's Section 42, better known as LIHTC (Low-Income Housing Tax Credit). Lowercase "a" affordable housing is housing that's affordable because of its price point, regardless of subsidy. NOAH (Naturally Occurring Affordable Housing), workforce housing (serving households around 80 to 120% of area median income, or AMI), manufactured housing, that kind of thing. This guide focuses on the LIHTC world (capital A), since that's the engine behind most new affordable rental housing in the U.S. Since 1986, LIHTC has financed roughly 4 million apartments and served over 9 million households (ACTION Campaign, as cited by NMHC; HUD's official LIHTC database places the figure at 3.7 million units placed in service through 2023).

Everyone touches everyone else. That's why it can feel overwhelming at first. But once you see how the pieces fit, the doors start to open.

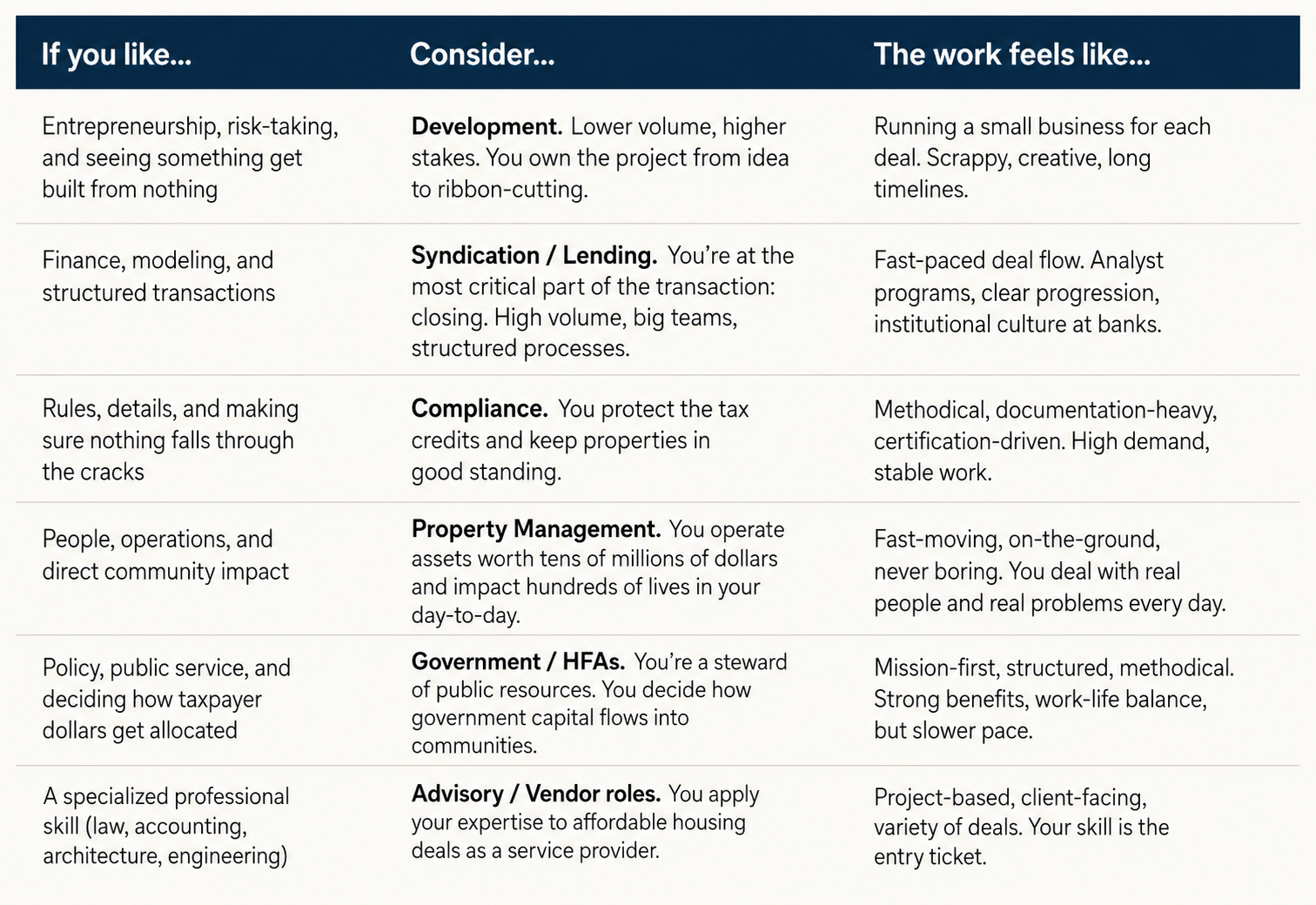

Which Affordable Housing Career Path Is Right for You?

Career Paths at a Glance

Development. Common entry roles: Development Analyst, Associate, Project Coordinator. Entry comp: $60K to $85K. Culture: entrepreneurial, smaller teams, long deal cycles, high autonomy.

Syndication / Equity. Common entry roles: Acquisitions Analyst, Investment Analyst, Fund Analyst. Entry comp: $60K to $80K. Culture: institutional, deal-driven, structured analyst programs, high volume.

Lending / Debt. Common entry roles: Production Analyst, Debt Analyst, Underwriting Analyst. Entry comp: $60K to $85K. Culture: bank culture, clear hierarchy, CRA-driven, relationship-focused at senior levels.

Property Management. Common entry roles: Leasing Consultant, Assistant Property Manager, Community Manager. Entry comp: $35K to $55K. Culture: fast-paced, on-site, resident-facing, tangible daily impact.

Compliance. Common entry roles: Compliance Specialist, Coordinator, Analyst. Entry comp: $45K to $70K. Culture: detail-oriented, process-driven, certification culture, high demand.

Government. Common entry roles: Program Analyst, Housing Specialist, HFA Underwriter. Entry comp: $50K to $95K. Culture: mission-first, structured, strong benefits and pension, steady pace.

Advisory / Vendor. Common entry roles: Staff Accountant, Associate, Analyst, Project Manager. Entry comp: $55K to $120K and up. Culture: client-facing, project-based, variety of deals, professional services culture.

A note on compensation: Compensation varies widely by market, employer type, experience level, and whether the role is at a bank, developer, syndicator, nonprofit, HFA, property management company, or consulting firm. The ranges below are meant to be directional, not exact. Geographic variation is significant. The same role in rural Alabama and New York City can differ by 40% or more. Figures are based on current job postings, public salary data, and sector knowledge. Use them as benchmarks for relative magnitude across roles, not as offers you should expect.

Affordable Housing Developers: The Builders

If you want to be closest to making housing happen, this is where the action is (I'm biased, since this is what I do for a living). Developers are the ones taking the risk. Buying land or properties, pulling financing together, and then either building something new or fixing up what's already there.

If you want to be closest to making housing happen, this is where the action is (I'm biased, since this is what I do for a living). Developers are the ones taking the risk. Buying land or properties, pulling financing together, and then either building something new or fixing up what's already there.

You'll find both nonprofit developers (Mercy Housing, BRIDGE) who are usually mission-first and rooted in community, and for-profit developers (Dominium, The NRP Group, Lincoln Avenue Communities) who still work inside the LIHTC system, just with a different bottom line. At the end of the day, both are trying to make the numbers work so homes get built and stay affordable.

New Construction vs. Preservation

Two main tracks live inside development, and they come with different deal dynamics and skill sets.

New construction means building from the ground up. Site identification, entitlements and zoning, design, tax credit applications, financing, construction, lease-up, stabilization. It's a multi-year process with more moving pieces and more risk, but also more creative control.

Preservation (sometimes called "acquisition-rehab") means buying existing affordable or at-risk properties and recapitalizing them with new LIHTC allocations, rehabilitation financing, and updated regulatory agreements. Preservation deals tend to move faster, have existing cash flow, and involve less construction risk. They come with their own complexities, though, around existing tenants, deferred maintenance, and layered financing. Both tracks are growing, and many firms do both.

Entry-Level Developer Roles

The entry role goes by a lot of names. Development Analyst, Development Associate, Project Manager, Project Assistant. They all cover the same core idea: supporting the full development process.

Smaller companies: You'll wear a lot of hats (a fancy way of saying "you do everything"). Site analysis, design coordination, financing, construction oversight, lease-up. You'll touch all of it.

Larger companies: The work is more specialized. Some firms split roles by discipline. One track leans finance-heavy (running numbers, pulling together financing, managing closings) and another leans construction-heavy (tracking budgets, schedules, contractors). Other firms split it by phase. You might handle everything from site selection through closing, then hand the project off to a construction or asset management team. Either way, your main job is project management.

Other roles you'll see at larger firms:

Capital Markets: Focused purely on financing and closings across the pipeline.

Asset Management: Focused on properties after they're built. Overseeing property managers, compliance, reporting, and investor relations.

Technical roles: Construction management, design management, owner's rep work.

Comp ranges: Based on current job postings and public salary data, entry-level Development Analysts typically fall in the $60K to $85K range. Mid-level Affordable Housing Developers generally land in the $70K to $125K range, with averages near $95K. Senior development directors and VPs at for-profit shops can earn $140K to $250K and up, often with upside through development fees and carried interest.

Big picture: Developers are the glue. If you like finance, real estate, and watching a spreadsheet turn into a building with people living in it, this is the lane.

This path may be a fit if you like: Entrepreneurship, creative problem-solving, and managing risk. Real estate finance and making the numbers work. Local politics, zoning, and community engagement. Seeing a project move from an idea to a physical building.

Work culture: Development is entrepreneurial. Teams tend to be smaller, deal cycles are long (2 to 5 years from concept to stabilization), and you wear a lot of hats. The pace can swing between intense (closings, application deadlines) and slower (entitlements, construction, waiting for the city to call you back). At smaller firms, expect high autonomy and broad responsibility. At larger firms, more structure but also more specialization.

LIHTC Investors and Syndicators: The Equity Side

This is the part of affordable housing that makes it different from every other corner of real estate. Here's the weird and wonderful thing about how this works.

This is the part of affordable housing that makes it different from every other corner of real estate. Here's the weird and wonderful thing about how this works.

Developers need equity. Cash upfront to help fund the project. In affordable housing, that equity usually comes through the sale of tax credits. The government gives developers tax credits as an incentive to build affordable housing. Those credits are basically coupons that reduce someone's federal tax bill, dollar for dollar, over ten years. Valuable, right? But developers don't need a tax break. They need cash. So they sell those credits to investors (mostly banks and corporations) for actual dollars upfront. That's the equity.

If that sounds convoluted, that's because it is. But it works, and it has worked since 1986.

Syndicators sit in the middle. They raise capital from investors, package it into funds, and deploy it into specific deals.

What's a fund? A fund is just a pool of money from one or more investors that a syndicator deploys across multiple deals. It spreads the risk and gives investors exposure to a diversified portfolio. Proprietary funds are raised for a single investor, usually tailored to that bank's CRA footprint and risk appetite. Multi-investor funds pool capital from many investors, which gives smaller institutions diversification they couldn't get on their own.

Types of LIHTC Syndicators and Investors

Dedicated syndicators: Independent, mission-driven groups whose entire business is affordable housing equity. Examples: Enterprise, National Equity Fund (NEF), CREA, Boston Financial, Ohio Capital Corporation for Housing.

Bank-affiliated syndicators: Equity platforms inside large banks, aligned with CRA goals. Examples: Bank of America, Wells Fargo, PNC, U.S. Bank, RBC Community Investments.

GSE investors: Both Fannie Mae and Freddie Mac are approved LIHTC equity investors, often focusing on underserved geographies or preservation deals.

Regional and nonprofit syndicators: Smaller, community-based funds with a regional footprint. Examples: Cinnaire, CAHEC, Midwest Housing Equity Group.

Direct investors: Some insurance companies and corporates (Aegon, MetLife, Prudential) invest directly, either through proprietary funds or as direct limited partners. Most entry-level roles are at syndicators, not at the investors themselves.

The LIHTC Syndication Process

The work falls into three main stages, plus a fourth track that's worth knowing about.

1. Front Office (Acquisitions/Investments): Sourcing and screening deals. Developers bring projects in once they've secured or are likely to secure tax credits, and the acquisitions team checks fit. CRA footprint, geography, returns, sponsor strength. Titles: Acquisitions Analyst, Investments Analyst/Associate.

2. Underwriting: The deep dive. Building financial models, reviewing due diligence (appraisals, market studies, partnership agreements), and preparing investment memos for internal committees. Titles: Underwriting Analyst, Investment Analyst/Associate.

3. Asset Management: After equity is invested, asset management monitors performance over the life of the investment. During the first 10 years, that includes overseeing the annual delivery (or "pay-in") of tax credits to investors. Through the full 15-year compliance period (and often beyond), the team tracks property operations, compliance, reserves, and investor reporting. Titles: Asset Management Analyst, Portfolio Analyst.

4. Investor Relations: Managing the relationship between the syndicator and its investors. Tracking fund performance, preparing investor reports and capital call notices, fielding questions about portfolio health. This is its own career track at larger syndicators, not just an on-ramp. Titles: Investor Relations Analyst, Fund Reporting Analyst, Director of Investor Relations.

Sidebar: Front office and underwriting roles are competitive. A lot of people start in Transaction Management (coordinating closings and diligence) or Investor Relations. Both are strong on-ramps into the equity side of affordable housing.

Comp ranges: Entry-level acquisitions and fund analysts at syndicators typically start at $60K to $80K. LIHTC underwriting analysts with a few years of experience generally land in the high five figures to low six figures. Senior VPs and directors of investor relations can earn $185K to $230K and up at major platforms.

Big picture: Development creates. Syndication matches the right investors with the right deals and protects the equity over time.

This path may be a fit if you like: Underwriting and financial modeling. Tax credits and structured finance. Working between developers and institutional investors. Portfolio-level risk analysis and investment memos.

Work culture: Syndicators and bank equity platforms are institutional environments. Structured analyst programs, clear progression tracks, high deal volume. Expect busy periods around closings and fund launches. The culture is more corporate than development but more mission-oriented than traditional finance. Dedicated (non-bank) syndicators tend to feel more like nonprofits. Bank-affiliated platforms feel more like, well, banks.

Affordable Housing Lenders: The Debt Side

If you've worked in banking or commercial real estate, this is probably the most familiar path on the list. Syndicators bring the equity, lenders bring the debt. The mechanics here look a lot more like traditional CRE finance than the equity side does. The deal structures, credit analysis, and underwriting principles translate directly, which makes this a natural entry point if you're coming from a banking or finance background.

Why Banks Lend to Affordable Housing (CRA in Plain English)

Banks don't lend into affordable housing purely out of goodwill. Why do they care? Short answer: they have to. The Community Reinvestment Act (CRA) requires banks to reinvest in the communities where they take deposits. Affordable housing is one of the cleanest ways to meet those obligations. Deals are large, relatively stable, and spread across geographies. That's why every major bank (Citi, Wells Fargo, JPMorgan, Bank of America, U.S. Bank) has a dedicated affordable housing lending team. CRA makes it a business priority, and developers need the capital, so the two sides keep each other busy.

Types of Affordable Housing Lenders

Banks: National players do deals across the country. Regional banks stick to their footprint. Banks provide construction loans, bridge loans, and permanent financing.

CDFIs (Community Development Financial Institutions): Mission-driven lenders that step in where banks might not. More flexible, often work with smaller or emerging developers. Examples: LISC, Enterprise Community Loan Fund, Capital Impact Partners.

Agencies (Fannie Mae, Freddie Mac, HUD/FHA): Government-backed programs that insure or purchase loans. Developers access them through "seller/servicers" (approved companies that originate loans on behalf of the agencies). That includes banks like Citi, Wells, KeyBank, and nonbanks like Walker & Dunlop, Berkadia, CBRE, JLL, Greystone.

Housing Finance Agencies (HFAs): State and local entities that provide tax-exempt bonds (government-backed financing that keeps borrowing costs low) and soft loan programs (low-interest or deferred loans). Examples: TDHCA in Texas, MassHousing in Massachusetts, NYC's HDC.

Lending Roles

The role structure mirrors the equity side (originations, underwriting, asset management) but the work is focused on debt. Sizing loans, analyzing cash flows, structuring construction-to-permanent financing, monitoring borrower performance after closing. Key titles: Production Analyst, Debt Analyst, Originations Analyst, Underwriting Analyst, Relationship Manager, Asset Management Analyst. Relationship Managers are particularly important on the lending side. They're the deal-sourcing, client-facing roles that don't have a direct equivalent in syndication.

Comp ranges: Entry-level lending analysts at banks typically start at $60K to $85K. Underwriting analysts with one to three years of experience generally land in the high five figures to low six figures. Relationship Managers and senior originators can earn well into six figures plus bonus. CDFI roles tend to pay slightly less but offer strong mission alignment and flexible work.

Big picture: Syndication brings in the equity. Lending decides whether the rest of the capital stack gets funded.

This path may be a fit if you like: Credit analysis and debt sizing. Borrower relationships and deal structuring. Traditional commercial real estate finance. A clear progression from analyst to relationship manager.

Work culture: At banks, expect a traditional corporate environment. Clear hierarchies, formal processes, CRA-driven deal flow. Hours are generally better than investment banking but ramp up around closings. CDFIs are more relaxed and mission-focused, with smaller teams and more flexibility. Agency lending (Fannie/Freddie/FHA) is process-heavy and regulatory, but stable.

Affordable Housing Property Management, Compliance, and Operations

Here's something I've learned on the development side. When you're getting financing for a deal, you'll typically get asked: who's your general contractor, architect, and property management company? Lenders and investors want to know the right expertise is in place. Affordable housing has nuances that require specialized knowledge. Income certifications, rent restriction compliance, layered reporting to multiple funding sources, familiarity with program rules like Section 42, HOME, and HUD. A market-rate property manager who's never dealt with LIHTC compliance is going to have a steep learning curve, and a more expensive one than they expect.

Here's something I've learned on the development side. When you're getting financing for a deal, you'll typically get asked: who's your general contractor, architect, and property management company? Lenders and investors want to know the right expertise is in place. Affordable housing has nuances that require specialized knowledge. Income certifications, rent restriction compliance, layered reporting to multiple funding sources, familiarity with program rules like Section 42, HOME, and HUD. A market-rate property manager who's never dealt with LIHTC compliance is going to have a steep learning curve, and a more expensive one than they expect.

Operations is also where every assumption you made in the proforma gets tested in real life. How quickly can you lease it up? What does stabilized vacancy look like? How much staff do you really need on site? These are the folks dealing with residents every day.

What They Do

Property management companies handle the day-to-day operations of affordable housing communities. They're the link between the building as a financial asset and the building as someone's home. The work includes leasing units and processing applications, verifying income and ensuring rents comply with LIHTC or other programs, coordinating maintenance and repairs, preparing compliance reports for lenders, investors, and agencies, and supporting residents through services or referrals.

Types of Employers

For-profit management firms that manage affordable portfolios on behalf of owners (Asset Living, WinnCompanies, The Michaels Organization).

Nonprofit housing operators, often managing their own developments (Foundation Communities, National CORE, Volunteers of America).

Public housing authorities, which directly manage or contract out management of their portfolios.

Some firms are vertically integrated (the developer and property management company under the same umbrella). Others outsource to a third party. In-house teams are more connected to the development side. Third-party firms give you exposure to a wider variety of owners and programs.

LIHTC Compliance: The Regulatory Engine

Compliance is the thread that runs through the entire ecosystem, and it's one of the most in-demand skill sets in the industry right now. Every LIHTC deal comes with a 15-year compliance period (often extended to 30 years). Why 15? That's the minimum the IRS requires a property to maintain its affordability restrictions in exchange for the tax credits. During that time, someone has to make sure the property follows strict rules around who can live there, what rents can be charged, and how everything gets documented.

And it's not just LIHTC. If a deal has HOME funds (a federal block grant for affordable housing), HUD project-based vouchers (rental subsidies tied to specific units), Section 811 (housing for people with disabilities), tax-exempt bonds, or state soft money layered in, each source comes with its own rules. Compliance professionals have to know how those programs overlap and where they conflict. It's a job that rewards people who enjoy reading the rules, and there are not enough of those people.

Compliance roles exist at developers (in-house teams), property management companies (centralized compliance departments), syndicators and investors (portfolio-level monitoring), third-party compliance firms (outsourced file reviews and audit prep), and state housing finance agencies (the regulators themselves).

Compliance Certifications

HCCP (Housing Credit Certified Professional): From NAHB. The most widely recognized LIHTC compliance credential.

C3P (Certified Credit Compliance Professional): From Spectrum Seminars. Well-regarded LIHTC-specific certification.

COS (Certified Occupancy Specialist): From NCHM. More HUD-focused, covering Section 8, Section 202 (elderly housing), and Section 811.

SHCM (Specialist in Housing Credit Management): From NAHMA. Required by many state HFAs as a supervisor-level certification.

You don't need these to get hired, but having one (or being willing to get one) makes you a much stronger candidate. Most employers will pay for the courses.

Entry-Level Property Management and Compliance Roles

Assistant Property Manager / Community Manager: Day-to-day operations, rent collection, resident communication, compliance paperwork. $40K to $55K entry.

Leasing Associate / Leasing Consultant: Marketing, applicant eligibility, move-ins, recertifications. $35K to $50K.

Compliance Specialist / Compliance Coordinator: File reviews, income calculations, audit prep, reporting. $45K to $70K, scaling to $70K to $85K and up with certifications.

Compliance Analyst: More common at syndicators and investors. Portfolio-level monitoring and reporting. $55K to $80K.

Compliance Monitor / Auditor: Typically at state HFAs. On-site inspections and file reviews. $50K to $75K.

Resident Services Coordinator: Connecting households to local resources, education, financial counseling. $38K to $55K.

Compliance Manager / Director of Compliance: Senior track. Overseeing compliance for a portfolio, managing a team. $80K to $120K and up.

Big picture: Development creates. Syndication funds the equity. Lending funds the debt. Property management and compliance sustain and protect it. And all of this work happens within a framework that government creates and enforces.

This path may be a fit if you like: Operations, people, and solving real problems on the ground every day. Rules, documentation, and detail-oriented work. A clear certification path with recognized credentials. Managing assets worth tens of millions of dollars and directly impacting hundreds of lives.

Work culture: Property management is fast-paced, on-site, and people-intensive. No two days are the same. You're dealing with residents, maintenance emergencies, inspections, and compliance deadlines all at once. Compliance roles are more office-based and methodical, with a documentation-heavy rhythm. Both paths offer stable demand and clear career progression, especially with certifications.

Government and Public Sector: Where the Programs Come From

Without government, none of this exists. There's no LIHTC program. There's no tax-exempt bond authority. There's no HOME or Section 8. Government creates the rules, allocates the resources, and monitors the results. If you're drawn to policy, public service, or being on the regulatory side of the table, this is a massive (and often overlooked) career path.

There's also a quiet upside nobody talks about. After spending a few years at an HFA or HUD, you understand how the rules are written, how applications get scored, and what the agencies care about. That kind of context is gold to developers, syndicators, and consultants. Government alumni get hired.

State Housing Finance Agencies (HFAs)

Every state has one. HFAs allocate 9% tax credits (through a competitive process governed by the state's Qualified Allocation Plan, or QAP), issue tax-exempt bonds for 4% deals, and provide soft financing. They also monitor LIHTC compliance on the back end, conducting physical inspections and file reviews. HFAs employ underwriters, compliance monitors, asset management officers, policy analysts, and program administrators. Examples: TDHCA (Texas), NCHFA (North Carolina), CalHFA/CTCAC (California), MassHousing, IHDA (Illinois).

HUD and Federal Agencies

The U.S. Department of Housing and Urban Development sets federal rules for programs like Section 8, HOME, Section 202, and Section 811. HUD employs portfolio administrators, housing program specialists, community planning and development specialists, and economists across 10 regional offices. The Federal Housing Finance Agency (FHFA) oversees Fannie Mae and Freddie Mac.

Local Housing Departments and PHAs

Cities and counties have their own housing departments that handle zoning, entitlements, local funding programs, and housing plans. Public Housing Authorities (PHAs) manage public housing and administer Housing Choice Voucher programs. There are approximately 3,300 PHAs nationwide (National Housing Law Project).

Entry-Level Government Roles

Program Analyst / Housing Program Specialist: Evaluating applications, monitoring programs, analyzing policy impacts. $55K to $80K at the state level. $60K to $95K at the federal level.

Compliance Monitor / Housing Inspector: Conducting on-site inspections and file reviews of LIHTC and HUD properties. $50K to $75K.

Underwriter (HFA): Reviewing LIHTC applications and bond deals for financial feasibility. $60K to $90K.

Policy Analyst: Researching housing needs, drafting policy recommendations, supporting legislative initiatives. $55K to $85K.

Community Development Specialist: Administering HOME, CDBG, and other federal grant programs at the local level. $50K to $75K.

Comp note: Government roles may pay 10 to 20% less in base salary than private-sector equivalents, but they often come with strong benefits, pension plans, job stability, and generous PTO. A lot of people build long careers in the public sector because of the mission alignment and work-life balance. Advancement can be slower at some agencies, but government experience is also a strong platform for later moves into development, syndication, lending, or consulting.

Big picture: Government sets the rules, allocates the resources, and holds everyone else accountable. If you want to shape the system rather than operate within it, start here.

This path may be a fit if you like: Being a steward of taxpayer resources and deciding how public capital gets allocated. Understanding how the rules are made and enforced. Reviewing applications and evaluating whether projects serve the public interest. Job stability, pensions, and genuine work-life balance.

Work culture: Government work is structured, mission-driven, and predictable. The pace is steadier than the private sector, with less crisis-mode energy. Benefits and pensions are strong. Advancement can be slower, but the policy exposure is unmatched, and government alumni are highly valued by developers, syndicators, and consultants.

Other Roles in the Affordable Housing Ecosystem

The sections above cover the core paths. But there's a wider universe of professionals who make affordable housing deals happen, and a lot of them are great entry points if you're already trained in something specific.

Accounting and tax advisory: Firms like Novogradac, CohnReznick, and Plante Moran handle cost certifications, tax credit delivery, and audit work for developers, syndicators, and investors. They also produce market studies and advisory reports. If you're a CPA or accounting-minded, this is a well-worn path into the industry. Entry-level staff accountants start around $55K to $75K. Managers and partners earn significantly more.

Housing attorneys: Affordable housing deals are legally complex, which is a polite way of saying a single closing can have ten attorneys in the room. Lawyers in this space handle partnership agreements, regulatory compliance, bond counsel work, tax opinion letters, and land use/entitlement issues. Firms like Nixon Peabody, Ballard Spahr, and Coats Rose have dedicated practices. Associates typically start at $80K to $120K and up.

Market study and appraisal firms: Most LIHTC deals require a market study and an appraisal as part of the application and financing process. Novogradac, CohnReznick, CBRE, and regional appraisal shops employ analysts who evaluate demand, comparable properties, and rent reasonableness. If you like research and data analysis, this is a solid niche.

Architects and design firms: Affordable housing has its own design considerations. Unit mix optimization, accessibility requirements (ADA, Fair Housing, UFAS), cost-efficient construction methods, community space programming. Firms that specialize in affordable multifamily (KTGY, Humphreys & Partners, Mithun) hire architects and designers who understand these constraints.

Construction management and general contractors: Every LIHTC deal has a construction phase, and affordable housing construction comes with its own requirements. Davis-Bacon prevailing wage compliance (on a lot of deals), environmental reviews, historic preservation constraints, phased construction in occupied buildings. Construction Project Managers in affordable housing generally earn in the high five figures to low six figures depending on project scale and market.

Environmental and engineering consultants: Phase I and Phase II environmental site assessments are required for virtually every deal. Civil engineers handle site plans, grading, and utility design.

Technology and software: Yardi (with its Voyager Affordable Housing module), RealPage (OneSite Affordable), and newer platforms are the backbone of property management and compliance operations. These companies hire implementation consultants, software developers, client services specialists, and compliance software analysts. Proficiency in Yardi or RealPage is now a core requirement for most PM and compliance roles. Yes, even if you hate it.

Advocacy and policy organizations: Groups like the National Low Income Housing Coalition (NLIHC), National Council of State Housing Agencies (NCSHA), and state-level advocacy orgs work on the policy side. Pushing for funding, defending programs, shaping the rules that everyone else operates under.

You don't have to be a developer or a lender to have a career in affordable housing. The ecosystem needs all of these players, and a lot of them are hiring.

Affordable Housing Careers: Frequently Asked Questions

Do I need a specific degree to work in affordable housing?

No. People come in from finance, urban planning, public policy, social work, accounting, and plenty of unrelated fields. What matters more is your willingness to learn the programs and deal structures. A finance or real estate degree is useful for development and lending roles. A public policy or planning background fits naturally at HFAs and nonprofits. None of it is strictly required. Plenty of senior people in this industry started with no housing-specific education, and figured it out on the job like everyone else.

What certifications are helpful for LIHTC and affordable housing careers?

For compliance, HCCP, C3P, COS, and SHCM are the most recognized credentials, and many employers require or strongly prefer at least one. For property management, the NAHP and CPO certifications are common. For development and finance roles, certifications matter less than deal experience, financial modeling skills, and program knowledge. Many employers will sponsor certification courses once you're hired.

What's the difference between a syndicator and an investor?

The investor is the entity putting up the money (usually a bank or corporation buying tax credits to reduce their tax liability and meet CRA obligations). The syndicator is the intermediary that raises capital from those investors, packages it into funds, and deploys it into specific LIHTC deals. The syndicator also manages the investment through the compliance period and handles reporting. Most entry-level equity-side jobs are at syndicators, not at the investors themselves.

How much do affordable housing jobs pay?

You can build a genuinely good career here. Entry-level analysts at banks and syndicators typically start at $60K to $85K. LIHTC underwriting analysts with a few years of experience generally land in the high five figures to low six figures. Senior developers and VPs can earn $140K to $250K and up, often with upside from development fees or carried interest. Directors of investor relations at major syndicators earn $185K to $230K and up. Compliance specialists start around $45K to $70K and scale meaningfully with certifications and portfolio-level responsibility. Property managers overseeing affordable communities earn $50K to $85K, with regional roles well over $100K. Government roles may pay 10 to 20% less in base salary, but the pension, benefits, and stability make the total package competitive. This is not a "low-paying do-gooder" field.

Can I transition into affordable housing from market-rate real estate or another industry?

Yes. If you're coming from market-rate real estate, you already speak the language of underwriting, deal structuring, and property operations. The learning curve is the subsidy layer. LIHTC, HOME, HUD programs, tax-exempt bonds, and the regulatory requirements that come with them. If you're coming from outside real estate entirely, compliance and property management are the most accessible entry points because they train you on the programs directly. The industry is growing and actively looking for smart people from diverse backgrounds.

What's the work-life balance like?

It depends on the lane. Development can be intense around closings and tax credit application deadlines, but the pace between deals can be more flexible, especially at smaller shops. Syndication and lending at banks tend to follow a more institutional rhythm. Busy during deal cycles, more predictable hours otherwise. Compliance and property management are generally 9-to-5 unless there's an audit or a crisis. Government roles are some of the most predictable in terms of hours. Across the board, affordable housing tends to offer better work-life balance than, say, investment banking or private equity, partly because the mission-driven culture discourages the "grind it at all costs" mentality.

Is affordable housing a good long-term career, or is it a stepping stone?

Both, depending on what you want. Plenty of people build 20- or 30-year careers entirely within affordable housing and reach senior leadership. Others use it as a platform. Lending experience translates to development. Syndicator experience translates to investor-side roles or consulting. HFA experience translates to the private sector. The skills are highly transferable because the ecosystem is so interconnected. Very few people who enter this industry regret it.

Glossary of Affordable Housing Terms

AMI (Area Median Income): The income benchmark HUD publishes annually for each metro area. Used to determine who qualifies for affordable housing programs and what rents can be charged.

CDBG (Community Development Block Grant): A federal program that provides annual grants to state and local governments for community development activities, including affordable housing, infrastructure, and economic development.

CDFI (Community Development Financial Institution): A mission-driven lender certified by the U.S. Treasury that provides financing in underserved communities.

Compliance Period: The period (typically 15 years for LIHTC, often extended to 30) during which a property must maintain affordability restrictions.

CRA (Community Reinvestment Act): A federal law requiring banks to reinvest in the communities where they take deposits. Affordable housing lending and investment is a primary way banks meet CRA obligations.

Due Diligence: The research and review process to verify everything about a deal checks out before money changes hands.

GSE (Government-Sponsored Enterprise): Fannie Mae and Freddie Mac. Federally chartered entities that support the mortgage market, including affordable housing loans.

HFA (Housing Finance Agency): A state or local government entity that administers affordable housing programs, allocates tax credits, and issues bonds. Examples: TDHCA, MassHousing, NCHFA.

HOME: The HOME Investment Partnerships Program. A federal block grant for affordable housing activities including new construction, rehabilitation, and rental assistance.

HOTMA (Housing Opportunity Through Modernization Act): Federal legislation enacted in 2016 that modernizes income and asset verification rules for HUD-assisted housing. Implementation has been phased through multiple HUD compliance extensions; the deadline for full compliance with the HOTMA final rule for multifamily owners is currently January 1, 2027, per HUD Notice H 2025-07 (HUD HOTMA page). Affects how properties calculate tenant income and eligibility.

LIHTC (Low-Income Housing Tax Credit): The largest source of affordable rental housing production in the U.S. (HUD). Comes in two flavors: 9% credits (competitive, awarded by state HFAs) and 4% credits (non-competitive, paired with tax-exempt bonds).

NOAH (Naturally Occurring Affordable Housing): Market-rate housing that is affordable due to its age, condition, or location rather than through government subsidies.

PHA (Public Housing Authority): A local government entity that manages public housing and administers Housing Choice Voucher (Section 8) programs. Over 3,000 exist nationwide.

QAP (Qualified Allocation Plan): The document each state publishes that governs how it awards competitive 9% LIHTC credits. The QAP sets scoring criteria, priorities, and application requirements. Understanding your state's QAP is essential for anyone in development.

RAD (Rental Assistance Demonstration): A HUD program that allows public housing authorities to convert public housing units to project-based Section 8 contracts, enabling access to private financing (including LIHTC) for rehabilitation.

Section 8 (Project-Based Rental Assistance): A HUD program providing rental subsidies tied to specific units. Tenants pay roughly 30% of income toward rent.

Section 42: The IRC section governing the LIHTC program.

Section 202: A HUD program that provides capital advances and project rental assistance for housing serving very low-income elderly households (age 62+).

Section 811: A HUD program that funds housing for very low-income people with disabilities.

Syndicator: A company that raises equity capital from investors, packages it into funds, and deploys it into LIHTC deals. Examples: Enterprise, NEF, CREA, Boston Financial.

Tax-Exempt Bonds: Bonds issued by HFAs where bondholder interest is exempt from federal tax, allowing lower borrowing costs. Commonly paired with 4% LIHTC credits.

Tax Credit Recapture: When a property falls out of compliance, the IRS can claw back previously claimed tax credits.

Underwriting: The process of analyzing a deal's financial viability and risk before deciding whether to lend or invest.

Where Do You Go From Here?

If you've made it this far, you have a solid map of the affordable housing landscape. Who the players are, how they connect, where the jobs sit, what they pay. That's more than most people have when they first start exploring this space.

Here's my honest advice. Don't overthink your first role. The beauty of this industry is that once you're in, you can move around. People who start in lending end up in development. People who start in compliance move into asset management. People who start at nonprofits end up at banks, and vice versa. The skills are transferable because the ecosystem is so interconnected.

The most important thing is to get your foot in the door, learn as much as you can, and figure out what part of the work energizes you. The rest will follow.

Ready to explore the field? Browse affordable housing jobs on the LIHTC Leaders Job Board, where we track roles across development, lending, syndication, compliance, property management, government, and more.

The U.S. has a shortage of roughly 7.2 million affordable and available rental homes for the lowest-income renters (NLIHC, The Gap 2026). That gap isn't closing on its own. The industry needs more smart, motivated people who want to do something about it. Whether you end up on the development side, the finance side, the operations side, or the policy side, the work you do in affordable housing will outlast you. Buildings stay standing. Families stay housed. Communities stay whole.

Welcome to the houser life.